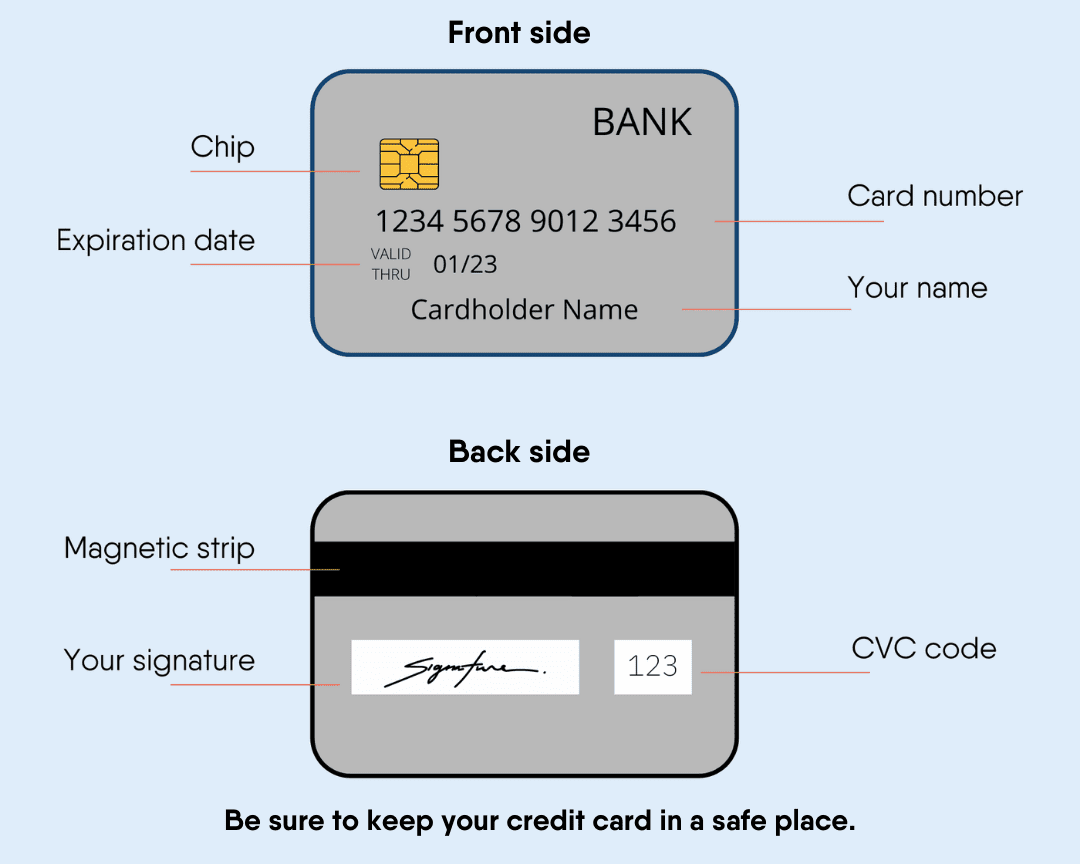

信用卡

美国有数百万人拥有信用卡。 人们在购物在线、支付昂贵物品或不想使用现金时使用信用卡。

信用卡使用方便、安全。 这些信用卡通常有消费限额,并要求每月向信用卡公司支付最低还款额。 请务必支付规定的最低还款额,否则将被收取滞纳金。

如果您没有向信用卡公司全额支付所有消费,您就会有余额。 信用卡余额通常会因利息而增加。 利息是信用卡公司为让您借钱而收取的额外费用。 余额被视为债务。

很多人的信用卡都有余额。 债务会给人带来压力。 重要的是,使用信用卡消费时要知道自己能在合理的时间内还清。

其他类型的卡片

您还可以使用其他类型的卡来代替标准信用卡。

开立担保信用卡需要存款。 最低存款额通常超过 40 美元,在某些情况下,这可以给你带来 200 美元的积分。 在账户开立期间,信用卡发卡机构持有这笔钱。 如果您按时还款,您就可以赚回押金并升级为普通信用卡。

这类卡可帮助您建立信用记录。

借记卡可以像信用卡一样使用。 您可以在开立银行账户或信用社账户后获得一张借记卡。 它不允许你借钱。 它只能使用您账户中的资金。 有时需要付费。

借记卡不能帮助你建立信用。 了解更多信息。

如果您没有社会保障号码来申请信用卡,有些公司可以接受您的个人纳税人识别号 (ITIN)。

对于没有社会保障号码的人来说,另一种选择是使用安全信用卡。

贷款

贷款是您借来的钱,必须连本带利归还。 贷款有很多种:个人贷款、发薪日贷款、商业贷款等。

贷款通常来自银行或金融机构。 他们会检查您的工作收入以及您是否拥有值钱的东西。 这有助于他们决定是否可以信任您偿还贷款。

按时还款将使您远离债务,并帮助您建立信用记录。

发薪日贷款适用于急需资金的人。 人们向贷款人借钱,是为了在拿到工资的当天还钱。

这些贷款也被称为现金预支贷款,通常收取高额利息。

有些发薪日贷款人使用非法手段,如过高的利息和不公平的条件。 请确保在签字前了解贷款的所有细节。

信用社提供发薪日替代贷款 (PAL)。 PAL 是一种短期贷款,因此您不必申请发薪日贷款。

您最多可以借到 1,000 美元,而且他们不会收取太高的利息。 在办理 PAL 之前,您必须成为信用社会员满一个月。

抵押贷款是人们买房时获得的贷款。 贷款机构会检查您的工作经历、信用评分、收入和其他因素,以确定您是否可以获得抵押贷款。 每个贷款机构都有不同的利率和选择。

申请抵押贷款可能很复杂。 最好向您的房地产经纪人或朋友咨询在哪里办理抵押贷款。 您需要许多文件,如联邦税表、工资单、银行对账单等。

联邦住房管理局 (FHA)提供有关抵押贷款和如何购房的资源。

永久居民(绿卡持有者)可以申请抵押贷款。 申请时,您需要提供在美国合法居留的证明文件。 您需要遵守银行或贷款人的要求。 所需文件包括

- 绿卡

- 护照

- 社会安全号码

- 最近的工资单

- W-2 表格

- 纳税申报

- 银行对账单

- 信用评分

永久居民也可以申请 FHA 贷款。 要求和条件与美国公民相同。

非永久居民也可以申请抵押贷款。 这个流程比较复杂。 申请人需要证明他们在美国的合法身份。 在大多数情况下,非永久居民必须出示国外收入。

助学贷款是为那些需要帮助支付学费的人提供的。 您以后必须连本带利还清。 贷款来自银行、金融机构或政府。 了解更多有关学生贷款的信息,并找到更多选择。

为移民和难民提供奖学金,帮助您支付教育费用。

这些贷款用于改善或创办自己的企业。 通常情况下,贷款人会为您规定非常具体的资金使用方式。

许多地方计划帮助难民和移民创办自己的企业,提供商业建议和资金讲习班。

寻求帮助

网站 | 提供 |

|---|---|

购房计划、小企业主贷款和难民储蓄计划 | |

信用社与银行类似,但属于非营利组织,由其成员所有。 他们更有可能向低收入者或无信用记录者提供贷款或信用卡 | |

为小企业、新企业和经济适用房建设提供贷款。 他们不想从服务中获利 | |

移民援助贷款,帮助您支付移民案件的费用 | |

向华盛顿特区、马里兰州、弗吉尼亚州和波多黎各的小企业主提供商业贷款(500 美元至 250,000 美元不等)。 | |

帮助社区更好地利用和了解信用社 | |

帮助您找到偿还信用卡债务的方法。 提供信用咨询和债务管理计划 | |

为美国小型企业提供 0% 利息的企业家贷款。 帮助服务不足社区的非营利组织 | |

为鼓励新罕布什尔州第一代移民的业务发展和创造就业机会而提供的贷款 | |

为信用记录有限或不熟悉金融机构的移民和难民提供贷款和商业咨询 | |

为美国移民和信用记录有限或为零的人提供贷款 | |

由小企业管理局担保的企业贷款 |

如何建立信用

申请信用卡或贷款需要有信用记录。 信用记录是您如何使用资金的记录。 它可以显示您是否使用过信用卡、是否有贷款、是否按时支付账单。

担保信用卡是开始建立信用的好方法。 按时支付电费和手机费等账单也有帮助。

信用记录中的信息会被记录到您的信用报告中。

信用报告包括个人和财务信息。 公司在向您贷款或批准您申请信用卡或抵押贷款之前,会使用这份报告来了解您的情况。 有时,雇主会在求职过程中要求提供这份报告。

根据您的信用记录,您会收到一个信用分数。 这个数字显示您的信用是好是坏。 高分是指 700 分及以上,低分是指 300 分左右。拥有良好的信用会让您在申请贷款或支付较少利息时有更多选择。

了解更多有关建立 信用记录的信息。

我们的目标是提供简单易懂和定期更新的信息。此信息不是法律建议。